How INSHUR Reduces Friction in the On-Demand Insurance Industry

Jun 25, 2026Written by Sabine VanderLinden

Inshur did not win Uber, Amazon, and DoorDash by building better insurance. It won by becoming fluent in their business models and embedding usage-based cover inside their operational flow. David Daiches, co-founder and COO of Inshur, argues that the next decade of insurtech belongs to companies that treat claims as the product, partnerships as distribution, and AI fluency as a survival skill. With over one million policies issued, 25 million Amazon Flex driving hours covered, and a USD 35M raise in 2024, Inshur is now building toward the hardest underwriting problem in mobility: autonomous fleets.

Three things to take away

- Inshur was born from a month of Manhattan Uber rides in 2016. The product insight came from drivers losing two weeks of income waiting for traditional broker-issued policies. Embedding insurance inside the platform onboarding flow turned a bottleneck into a growth lever.

- Insurance consumes roughly 25% of on-demand platform revenues, making it the single largest operational cost lever after labor. With over 10 million Americans participating weekly in the on-demand economy (Inshur internal data referenced in episode), and around 80% of them working across multiple apps, a single on-demand insurance wallet becomes infrastructure, not a product.

- Inshur brought claims operations in-house after realizing third-party administrators were undermining the customer experience. Daiches now describes claims as "the product" itself, with everything else being the delivery mechanism. AI is being deployed to empower adjusters, not replace them.

How Inshur Was Built: From Manhattan Back-Seat Research to Embedded Infrastructure

Inshur’s product strategy was set by one decision: spend a month inside the actual customer’s day before writing any code.

In 2016, David Daiches and co-founder Dan Bratshpis spent the best part of a month climbing in and out of Manhattan Ubers. Every five-minute ride, the same question to the driver.

"How do you buy your insurance?"

The answers exposed a generational mismatch that the entire insurance industry had missed. The 50-something Yellow Cab drivers were happy to visit a broker on a Tuesday afternoon and chat with Fred in accounts. The new Uber drivers lived on their phones, could not afford to lose two weeks of income while waiting for paperwork, and had no interest in walking into anyone’s office.

That month produced the founding insight of Inshur. The product was not better insurance. It was insurance that fit inside the way the new on-demand workforce actually operated, especially in the gig economy of short-term jobs, freelancers, and independent contractors. Nearly ten years on, Inshur operates across the US, the UK, and the Netherlands, has issued over 1 million policies, and counts Uber, Amazon, and DoorDash among its embedded partners.

Why This Matters Now: The Gig Economy and On-demand Economy Are No Longer Side Hustles

The on-demand economy has crossed from supplementary income into critical workforce infrastructure, and traditional annual policies are structurally incompatible with how those workers actually earn.

According to figures Daiches cites in the episode, over 10 million people in the US regularly participate in the on-demand economy. Roughly 40% of teachers and 70% of nurses use on-demand platforms to supplement their income. This is no longer a market for students and side hustlers. It is millions of working adults building post-COVID income resilience across multiple apps.

The implications for insurers are structural, not cosmetic. Annual policies designed for a single vehicle, a single use case, and a single employer cannot price risk for a worker doing 20 hours a month for Amazon Flex on Monday, six hours of Uber on Friday, and three DoorDash deliveries on Sunday. McKinsey’s Global Insurance Report and Swiss Re Institute sigma analyses have repeatedly flagged usage-based and embedded models as the only viable architectures for this segment, with clear benefits for carriers and platforms alike. Flexible coverage also helps platform companies retain talent while providing an added layer of protection for independent contractors.

This is the Frontier Firm gap in mobility insurance. The data exists. The platforms exist. The product architecture, for most carriers, does not.

The Four Insights That Reframe How Insurtechs Should Be Built

1. Fluency In The Partner's Business Model Beats Feature Parity Every Time

InsurTechs that win enterprise platform deals do not lead with technology demos. They lead with operational diagnosis.

Daiches is unambiguous about why Inshur won Uber when it was a 30-person startup competing against far larger incumbents.

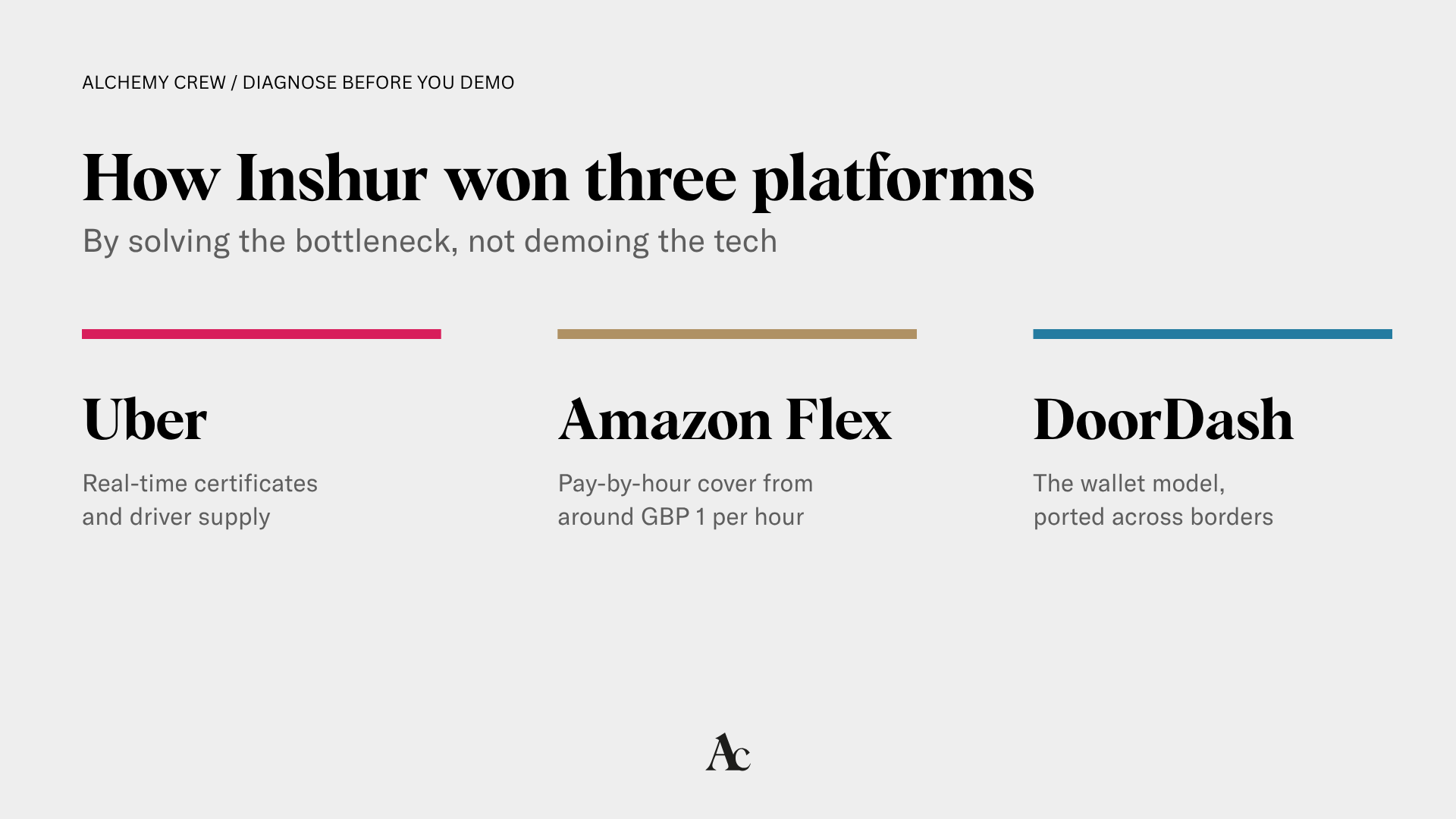

“It wasn’t just about selling insurance, it was about understanding the business model of the platforms and where their bottlenecks were. We approached it rather than going in demoing, we’ve got great technology. What we wanted to do was demonstrate that we understood what problems they were facing.”

For Uber, that meant driver supply, real-time certificate issuance to address uninsured drivers in the UK, and onboarding speed. For Amazon, it meant pay-by-hour cover starting around GBP 1 per hour to make Amazon Flex economically viable for drivers doing 20 hours a month. For DoorDash, it meant porting the wallet model across borders.

This is the Venture Client Model thesis from the platform side. Venture-clienting lets corporates buy, test, and adopt startup solutions now, aligned with a defined business need, so they can implement change with operational impact instead of waiting for equity returns. The DIVAAA framework—Discover–Investigate–Validate–Adopt–Activate–Amplify—is a repeatable process that reduces legal and financial drag during adoption. The partner is not buying a product. They are buying a solution to a constraint that is throttling their own growth.

2. Claims Are The Product. Everything Else Is The Delivery Mechanism.

Inshur outsourced claims in its early years and damaged its customer experience. Bringing claims in-house was the inflection point that turned Inshur from an insurtech vendor into a long-term platform partner.

The moment Daiches describes most viscerally is not the Manhattan rides. It is his own pre-insurance experience as a customer, when his parked car was hit, and his policy turned out to be practically useless once the GBP 500 excess, three-week repair queue, and inadequate courtesy car emerged.

“That experience stayed with me. We quickly realized that the TPA provided a poor experience for our customers. The product that we sell is claims. It’s the promise to sort things out when things go wrong. No matter what kind of fancy UIs you’ve got and marketing campaigns and slick websites, when the worst happens to people, we want them to be confident that they are covered.”

The strategic implication runs deeper than service quality. Owning claims gives Inshur a data backbone for better pricing, direct control over the customer satisfaction signal, and an operating advantage when platform partners measure driver downtime. Claims-driven value reduces driver downtime and creates a better embedded user experience than traditional sellers. Daiches frames it bluntly: claims are the product, and everything else just gets us to that point, including how quickly a team can respond when something goes wrong.

This is Intelligent Layers as a competitive moat. The intelligence core only generates insight if the data pipeline runs end-to-end through your own organization.

3. Autonomous Vehicles Will Rip Up The Underwriting Rulebook, And The Winner Builds The Arbitration Layer

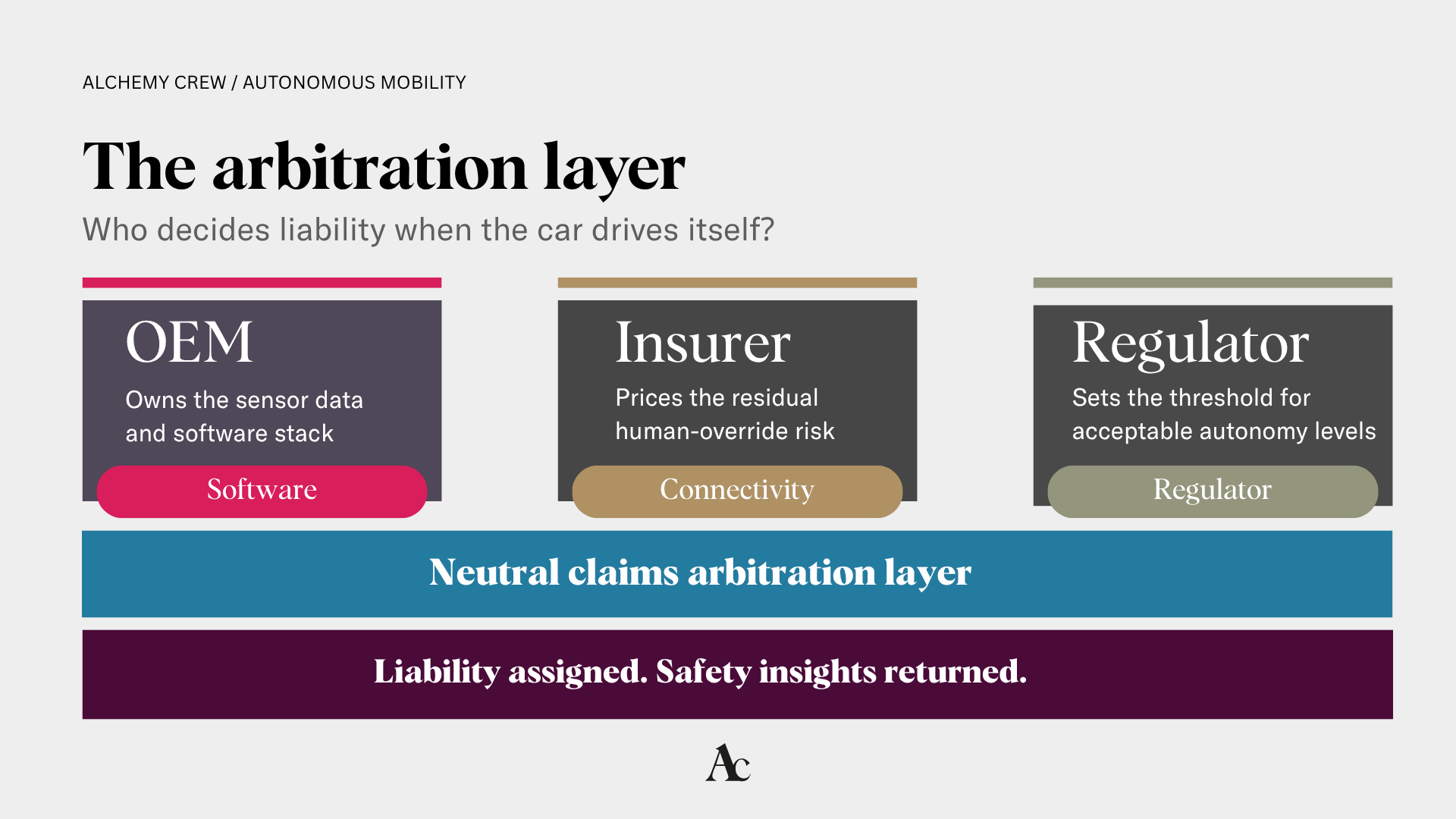

Ensuring autonomous fleets is not an extension of motor insurance. It is a new ecosystem-level underwriting problem that requires neutral arbitration across OEMs, software providers, fleet operators, and regulators.

Daiches describes autonomous vehicle insurance as the unworked problem of the next decade.

"Now you're having to ensure an ecosystem of vehicles, software, sensors, connectivity, fleet owners, and robotaxi platforms. There's an opportunity there because many people are developing their own systems and standards. There's an opportunity for some kind of autonomous vehicle liability profiling to sit in the middle of all this."

Inshur is exploring a claims arbitration service that pulls sensor data, LiDAR, telematics, connectivity logs, weather, and urban context to reconstruct incidents and assign liability across a complex stakeholder map. The commercial case is concrete. Litigation can account for up to 40% of motor claims costs in some markets, according to industry analyses. A neutral arbitration layer that reduces legal expense and feeds safety insights back to regulators could become foundational mobility infrastructure.

This is the agentic frontier of mobility insurance. The hardest underwriting challenge is the hybrid period: autonomous, driver-assisted, and human-driven vehicles sharing the same road, with liability questions that no current product can answer cleanly.

4. AI Fluency and Building with AI Agents Is Now a Survival Skill, And The Path is To Build, Not To Read Reports

Daiches, a former coder turned COO, has returned to building applications inside Inshur using Claude. His position is that any leader who is not personally building with AI will be making decisions from a position of theoretical knowledge in a market that demands operational fluency. Agentic AI is a subset of artificial intelligence comprising autonomous, goal-directed systems capable of determining actions and acting with minimal human intervention.

“I started as a coder. I’m now building my own stuff again on Claude. I’m absolutely loving it. If you want to be speaking from the position of having read a load of reports, I wouldn’t. I do this every day and on the weekend. I’ve built these apps that we’re using in the business now.”

His message for hiring and skills runs in two directions.

- For young people: get AI skills through self-teaching, then go work somewhere with traditional processes and low AI adoption, because that is where the value gap is largest.

- For incumbents: invest at least eight hours a week in self-learning, build small things, and avoid being the least AI-skilled person in an increasingly AI-native company.

Gartner predicts that by 2028, 33% of enterprise software applications will include agentic AI, enabling 15% of day-to-day work decisions to be made autonomously. Leaders should expect rapid adoption.

This is the Frontier Firm operating principle applied to talent strategy. Human-led, agent-operated companies are built by leaders who personally understand how to implement AI agents across insurance functions, from product development and software development to workflow automation. Managers need the feedback to develop with the process, as these systems are still in the early stages, but will evolve quickly through the next wave of transformation and technological evolution.

What Insurtech Founders and Insurance Industry Platform Leaders Should Consider This Upcoming Quarter?

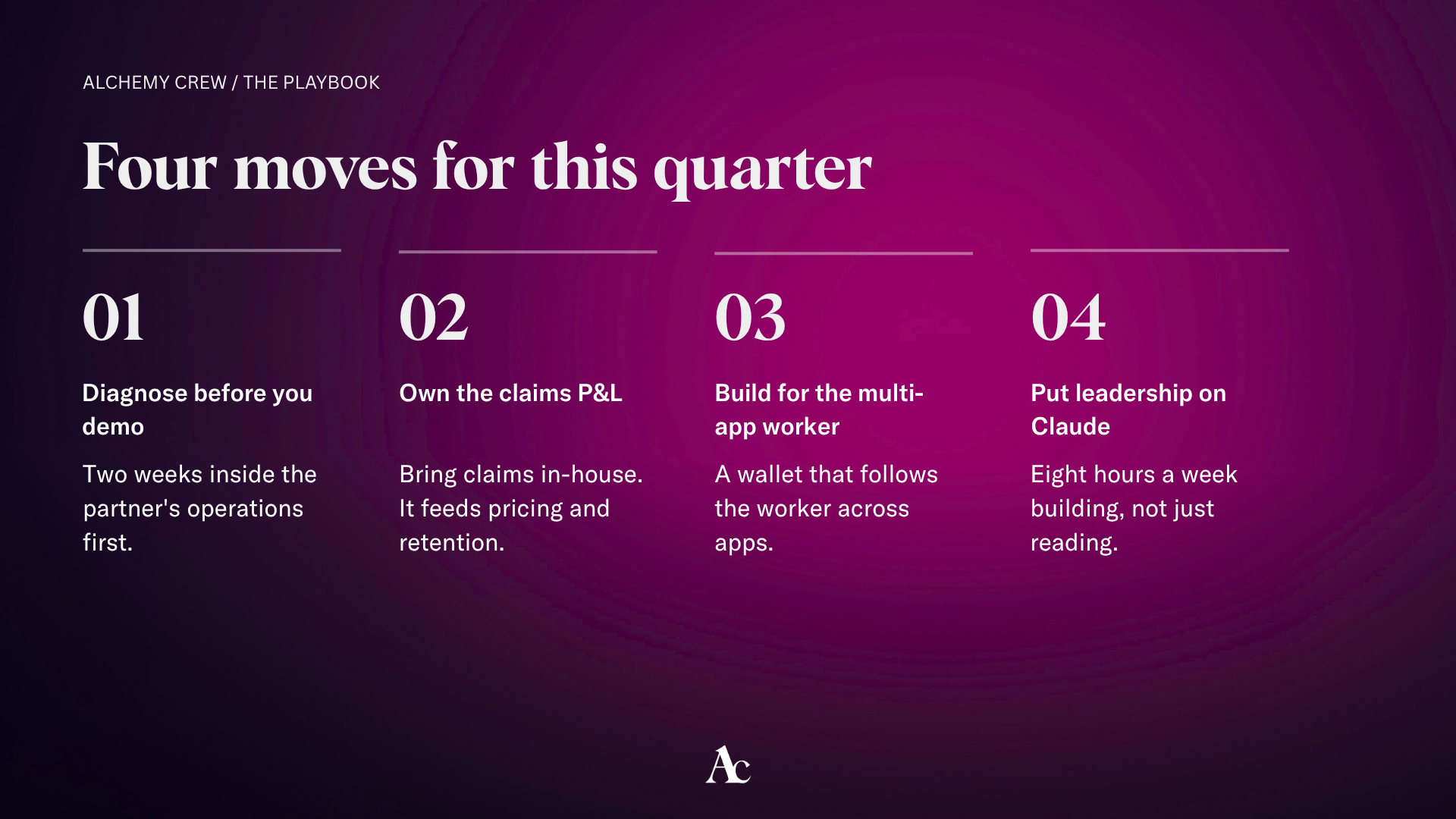

Four moves. Map the partner's bottleneck before the demo, own the claims P&L if claims management has become a strategic asset for you, build for the multi-app worker, and put your leadership team on Claude.

- Diagnose before you demo. Scaleups... Before any platform partnership pitch, spend two weeks inside your partner's operational reality. Identify the specific bottleneck in their business model that is throttling growth due to insurance. Lead the conversation with that diagnosis, not your technology stack.

- Bring claims in-house, even if it slows growth. From my chat with David (and other InsurTech MGA leaders), I learned that outsourced claims will undermine the customer experience and starve the pricing engine of data. You can facilitate this by leveraging other insurtechs solutions. The short-term operational cost is repaid in retention, partner trust, and underwriting intelligence.

- Design for a multi-app reality. Around 80% of on-demand workers operate across multiple platforms. Build wallet-based products that follow the worker across apps rather than locking coverage to a single platform contract.

- Mandate AI building, not just AI awareness, across leadership. Set an eight-hour-per-week minimum for senior leaders to personally build applications using tools like Claude. Decisions about AI strategy made without hands-on fluency will systematically underestimate both the opportunity and the operational change required.

The courage question for insurtech founders

The gap between insurtechs that scale to one million policies and those that stall at five thousand is not a technology gap. It is a fluency gap. Daiches and the Inshur team won Uber, Amazon, and DoorDash because they walked into every conversation understanding the partner's business model better than the partner expected.

The next decade of mobility insurance will be defined by whoever cracks the autonomous arbitration problem and whoever owns the on-demand wallet. Both are infrastructure plays. Both require the same posture: diagnose before you demo, own the data, and build before you opine.

Listen to the full conversation with David Daiches on Scouting for Growth

Which platform's business model are you fluent in, and which are you still demoing to?

Want to talk about it. Just set up a call with me here.

Frequently Asked Questions (FAQs)

What is embedded usage-based insurance in the on-demand economy?

Embedded usage-based insurance is a cover that sits inside a platform's onboarding and operational flow, charging drivers only for the hours or trips they actually work. Inshur's pay-by-hour Amazon Flex product, starting around GBP 1 per hour, is a working example. It replaces the annual policy model that made on-demand work economically unviable for part-time drivers.

Why does Inshur describe claims as "the product"?

Customers only experience the value of insurance when something goes wrong. Inshur brought claims in-house after realizing that third-party administrators were delivering a poor customer experience and depriving the company of the data needed for better pricing. Owning claims also serves platform partners, who need drivers back on the road as quickly as possible.

How will autonomous vehicles change motor insurance?

Autonomous vehicles shift the underwriting question from the human driver to an ecosystem of OEMs, software providers, sensor manufacturers, connectivity providers, and fleet operators. Inshur is exploring a neutral claims arbitration service that pulls sensor, telematics, and connectivity data to reconstruct incidents and assign liability, potentially reducing the litigation costs that can consume up to 40% of claims spend.

What skills should young people build to work in insurtech in 2026?

David Daiches recommends self-teaching AI skills using free resources like Anthropic's Claude 101 course, then applying those skills inside traditional industries where AI adoption is low. The value gap is largest in companies with mature processes and limited AI fluency, not in marquee AI startups.

References

Inshur company data (one million policies, 25 million Amazon Flex hours, USD 35M 2024 raise)

McKinsey Global Insurance Report on embedded and usage-based insurance

Swiss Re Institute sigma research on the protection gap and emerging mobility risks

Anthropic Claude 101 course referenced by David Daiches

McKinsey research on human-agent ratios and the future of work, referenced by Sabine VanderLinden

World Economic Forum Future of Jobs Report 2025

Microsoft Work Trend Index 2025, Frontier Firm framework

Editor in Chief

Rebuilding Risk Resilience