The Intelligence Layer In InsurTech Moved Into the Customer's Wallet

Jun 14, 2026Written by Sabine VanderLinden

Let's start with a question: where is the insurer-customer relationship heading?

Honestly, out of standalone apps and into the native mobile wallet. Drawing on a conversation with Gigasure founder Ernesto Suarez and Wallet Studio co-founder Marc Lampe, this article explains what wallet-native insurance is and why it matters now that AI agents are starting to buy on customers' behalf.

Three things to take away before you read further

- 35,000+ digital wallet cards created in under four months. Approaching 60% adoption. Five-star Trustpilot reviews tied to a single design move. Travel insurance has quietly become the unlikely lab for what's coming next in customer engagement.

- 88% of insurance customers cannot find their documents at the moment of claim. The Protection Gap is no longer just a coverage problem. It is an access problem, and the customer's wallet is where it gets solved.

- The app era is over. The next customer layer for insurance is wallet-native, parametric, and on its way to being agent-bought. The Intelligence Layer has just moved into the consumer's pocket, and the insurers ready for the Agentic Frontier are already shipping there.

The hospital scene that should keep every Chief Customer Officer awake about customer experience

Imagine you are lying in a hospital bed. You are bleeding. You are in a country you do not live in. And the doctors will not begin treatment until you provide proof of insurance.

You cannot find it.

That is the moment 88% of consumers describe at the point of claim. Not coverage. Not premiums. Access. Marc Lampe and Ernesto Suarez made plain why the Intelligence Layer in insurance is not a back-office story. It is a customer-pocket story.

The 88% figure comes from a census-wide survey of 2,000 consumers commissioned by Gigasure. It reframes a decade of customer experience theatre in one number. And it explains why a Berlin scaleup with $8M in seed funding and a London MGA with one previous exit have just shipped, together, what the industry has been talking about for ten years and shipping for roughly ten minutes.

Why this matters now: the 35,000-card stake in the ground

The numbers are not subtle. In under four months, the Gigasure × Wallet Studio partnership generated more than 35,000 digital wallet cards. The number is now north of 50,000. Adoption is approaching 60%. Customers cite the wallet card by name in their five-star reviews. The deployment went from kickoff to live in weeks, not the eighteen-month, "next free slot is January 2027" cadence Marc describes inside the average Fortune 500 insurer.

This is not a wallet feature. This is the first customer-facing Intelligence Layer the insurance industry has shipped at speed. And it is rewriting where the insurer-customer relationship lives.

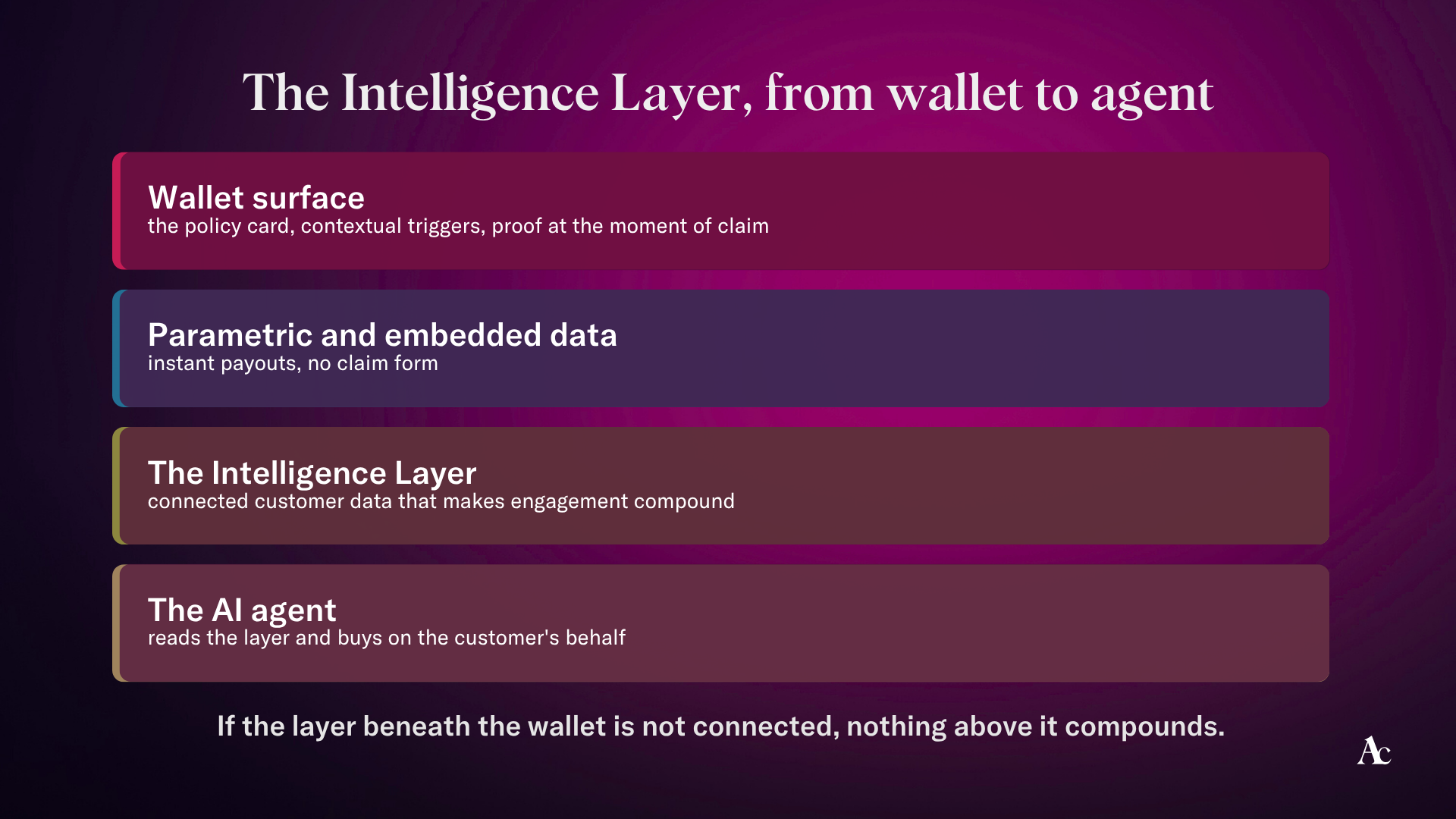

What is the Intelligence Layer for insurance risk management?

The Intelligence Layer for insurance is the persistent, wallet-native customer surface that connects policy, claim, payment, and contextual data in one place on the customer's phone. It replaces the failed app-as-front-door model with the layer the customer already opens daily, for boarding passes, loyalty cards, and payment credentials. It is the architecture that makes wallet-native insurance and agentic distribution commercially possible.

The app era is over, and Marc Lampe has been quietly proving it for a decade

Marc started his first company at seventeen. Exited at twenty-one. Spent time inside Deutsche Bank in Luxembourg, what he calls "an offshore island where you can see every department on every floor," before co-founding Miss Moneypenny Technologies and the Wallet Studio platform, now live with twenty-two insurers across Europe, including Zurich, ERGO, and SIXT.

The through-line across every venture is the same one: customer-facing, friction-removing, revenue-positive. The thesis behind Wallet Studio is the same, too. Only the architectural argument has hardened.

The argument is this. Native mobile wallets (Apple Wallet, Google Wallet) are the surface that customers already open multiple times a day. Boarding passes. Coffee at the airport. Loyalty cards. Hotel keys. The customer has been trained by Apple and Google and has 20 years of muscle memory to look in one place for what they need at the moment. Increasingly, that surface is backed by AI integration and the right tools, improving operational efficiency and cutting troubleshooting time from hours to minutes.

The insurer app has not earned that place. It cannot. The economics of getting a low-frequency insurance product installed, retained, and reopened do not exist, and never will. That is why incumbent customer engagement appears invisible to the customer. The product is there. The customer cannot see it.

Wallet-native engagement inverts that problem. The Intelligence Layer is not where the insurer wants the customer to go. It is where the customer already is. Underneath, agents extend that model to act like AI coworkers, completing complex tasks such as running code and managing files across local and cloud environments.

The 35,000-card proof point, and why a founder-led MGA with valuable insights got there first

Ernesto Suarez has been in insurance for twenty-five years. He sold Halo Insurance to Zurich in 2017, took notes instead of a holiday, and launched Gigasure in 2024, backed by SiriusPoint and AmTrust, with one declared ambition. Become the travel insurance customer's actual companion, not just their policyholder.

He met Marc at InsurTech Insights. The aha moment, in his words, was instant. "I went straight up to Marc and said, look, I'm building a digital-first MGA. I can be your experiment."

The deployment that followed did three things that the rest of the industry should study, and this kind of venture-clienting works because it starts with a clear business need.

It compressed the procurement clock. Marc describes the entire purchasing process as "literally three email threads." No siloed legal, IT, security, and procurement queues. No twelve-month integration plan. One MGA founder with full decision authority. One platform with the engineering depth to run integration, commercials, and compliance work in parallel rather than sequentially.

It produced numbers the corporate side cannot ignore. 35,000 cards in under four months, ~60% adoption, five-star reviews tied to the GigaCard, parametric flight-delay and baggage-delay triggers paying directly into the customer's bank account. No claim form, no waiting.

And it surfaced the strategic insight worth more than the metric itself. The Frontier Firm moves through ecosystem speed, not feature parity. An Intelligence Layer can support scenario modeling to test business strategies risk-free, use real-time analysis to track live changes across customer journeys, and help organizations keep focus on the key drivers of success. It can also create personalized recommendations, including optimal pricing models, for companies and partners managing change across the business. Gigasure did not build the wallet layer. Wallet Studio did not build the travel MGA. The advantage lies in the combination and in the willingness to ship it.

That is what the Frontier Operating Model looks like in practice. Not a feature roadmap. A network of best-in-class enablers stitched together by a founder with the conviction to move now, then expand as the future and management demands become clearer.

When the agent buys the policy, the Agentic Frontier for distribution

Marc described Wallet Studio, in conversation, as "the customer layer of the AgentIQ enterprise." It is the line that should keep every Chief Customer Officer in insurance up at night.

The reason. Distribution is about to change shape again. Not by 2030. By the next renewal cycle.

When an AI agent (Claude, ChatGPT, Gemini, an Apple Intelligence agent your customer never explicitly chose) books your customer's next trip, the same agent will buy the insurance. It will not visit your website. It will not download your app. It will negotiate, compare, and bind through APIs and wallet handoffs. The product that wins is the product the agent can read, parse, trigger, and prove to the customer in one place.

That place is the wallet.

The Agentic Frontier is not a 2030 narrative. It is a 24-month distribution shift. And it has a hard prerequisite. The insurer must already have a wallet-native, parametric, machine-readable customer layer, the Intelligence Layer, before the agent shows up to buy.

The MGAs are already there. The platforms are already there. The window for incumbent insurers to be ready is the window between this quarter and the next renewal season.

Frontier Firm versus pipeline-full

Marc puts it simply. Inside the Fortune 500 insurer, the answer is rarely "no." It is "we are excited, but our next free slot is January 2027."

The Frontier Firm answer is three email threads, parallel work-streams, and live in weeks.

The cost of the corporate pace is not the project. It is the compounding gap. Every quarter the incumbent waits, the Frontier Firm MGA ships, learns, and optimizes, and earns the trust the incumbent had budgeted to win two roadmaps from now.

The playbook: five moves for the next 90 days

For Chief Customer Officers, Chief Claims Officers, Chief Innovation Officers, and the CEOs of founder-led MGAs:

-

Audit your access gap, not your coverage gap. Survey your top two products. Ask the 88% question. At the moment of claim, can your customer find the documents, the number, and the proof? If the answer is no, your Protection Gap is access, not premium.

-

Choose one wallet-native pilot. Scope it in weeks, not quarters. One product. One customer journey. Wallet-native end-to-end. Use the speed itself as the experiment.

-

Map your Intelligence Layer. Where does your customer data live? Where do contextual triggers fire (flight, location, renewal, claim)? Wallet-native engagement only compounds if the layer beneath it is connected.

-

Pick the platform, not the project. Twenty-two insurers and a founder-led MGA chose the same Wallet Studio platform. They did not pick a vendor. They picked an architecture. The Intelligence Layer is a platform decision.

-

Make the partnership decision the way Ernesto did. Three email threads. Full decision authority. Parallel work-streams. If your governance cannot support that cadence on one pilot, the governance is the bottleneck, not the technology.

The stakes, reframed

In 90 days, one of two things will be true.

Either your customer's wallet contains your policy card, your contextual triggers, your parametric payouts, and the proof they need at the moment of claim, or the next agent to buy on their behalf can read it.

Or it does not. And the agent buys somewhere else.

The Intelligence Layer is a competitive layer. The window is open. The cost of standing still is the customer.

One conversation

Forty-five minutes. One conversation. A clear view of where your customer experience stands against the Wallet Studio × Gigasure benchmark, and what a 90-day wallet-native pilot looks like inside your own Frontier Operating Model.

Make sure to

- Download the Gigacard from Gigasure

- Evaluate Miss Moneypenny's embedded wallet technologies, delivering an AI-native customer experience infrastructure.

Frequently asked questions

1. What is wallet-native insurance for existing customers?

Wallet-native insurance is insurance distributed, surfaced, and serviced inside the customer's native mobile wallet (Apple Wallet or Google Wallet) rather than inside a standalone insurer app. Today, 66% of global financial organizations already offer integrated insurance services as added service value across their customer journeys. That momentum matters for business adoption: 81% of financial executives see embedded insurance as essential, and over half of financial firms expect it to contribute 10% of revenue within three years. The policy lives as a digital wallet card. The back of the card carries contact details, claim initiation, parametric triggers, and renewal prompts. It removes the customer's biggest friction at the moment of claim: finding the documents.

2. What is the Intelligence Layer for insurance, and how is it different from a customer portal?

The Intelligence Layer is the persistent, machine-readable, customer-facing surface that connects policy, claim, payment, and contextual data, aggregates information from varied databases, and exposes that knowledge to the customer (and, increasingly, the customer's AI agent) in one place on the phone. A customer portal is a destination the customer rarely visits. The Intelligence Layer is the surface that the customer already opens every day. That difference is the entire commercial argument.

3. Why is mobile wallet adoption rising faster than insurer app adoption?

Because the customer already uses native mobile wallets for boarding passes, payment cards, and loyalty credentials. The behavior is learned. Consumers still trust established brands more than digital-only banks, which gives incumbents an opening if they make insurance easier to access. The friction is zero. Insurance apps require install, retention, and re-engagement against a low-frequency product, a battle the economics will not support. Wallet-native insurance inherits the customer's existing habit instead of trying to build a new one, helping users access cover with clear benefits that protect them against everyday risks. Over 50% of consumers feel underinsured against modern-day risks, which makes low-friction wallet access more relevant. Gigasure's data, approaching 60% adoption in under four months, confirms the pattern.

4. How does a partnership like Wallet Studio × Gigasure shorten time-to-market for new propositions?

By compressing procurement, decision-making, and integration into a single chain of accountability. Ernesto Suarez describes the entire purchase decision as "three email threads." Marc Lampe and his team run integration, legal, and commercial workstreams in parallel rather than sequentially. Rollout can then manage a clear DIVAAA progression through Discover, Investigate, Validate, Adopt, Activate, and Amplify. Objective data points help reduce bias when deciding, for example, what to launch and how to optimize time-to-market. The result is a kickoff-to-live cadence measured in weeks, not the eighteen-month corporate procurement standard, and it is the shape of the Frontier Operating Model for insurance distribution.

5. What does the Agentic Frontier mean for insurance distribution?

The Agentic Frontier is the shift from human-purchased insurance to agent-purchased insurance, in which AI agents (booking the trip, the rental car, the appointment) negotiate and bind the policy on their behalf. For insurers, the prerequisite is a machine-readable, wallet-native customer layer that the agent can read, parse, and prove to the human, with defined identity, control, and management guardrails inside the enterprise before they can do real work safely. Without that layer, the insurer is invisible to the agent who bought the trip, and the same intelligence layer helps employees and customers trust the job those agents perform.

Editor in Chief

Rebuilding Risk Resilience