AI Horizon 2030: Agentic Insurance & the Readiness Problem

Jul 08, 2026

Written by Sabine VanderLinden

Nine months after AI Horizons 2030, the diagnosis is confirmed. Pilots don't scale — operating models do. So what do the other four in five insurers do?

-

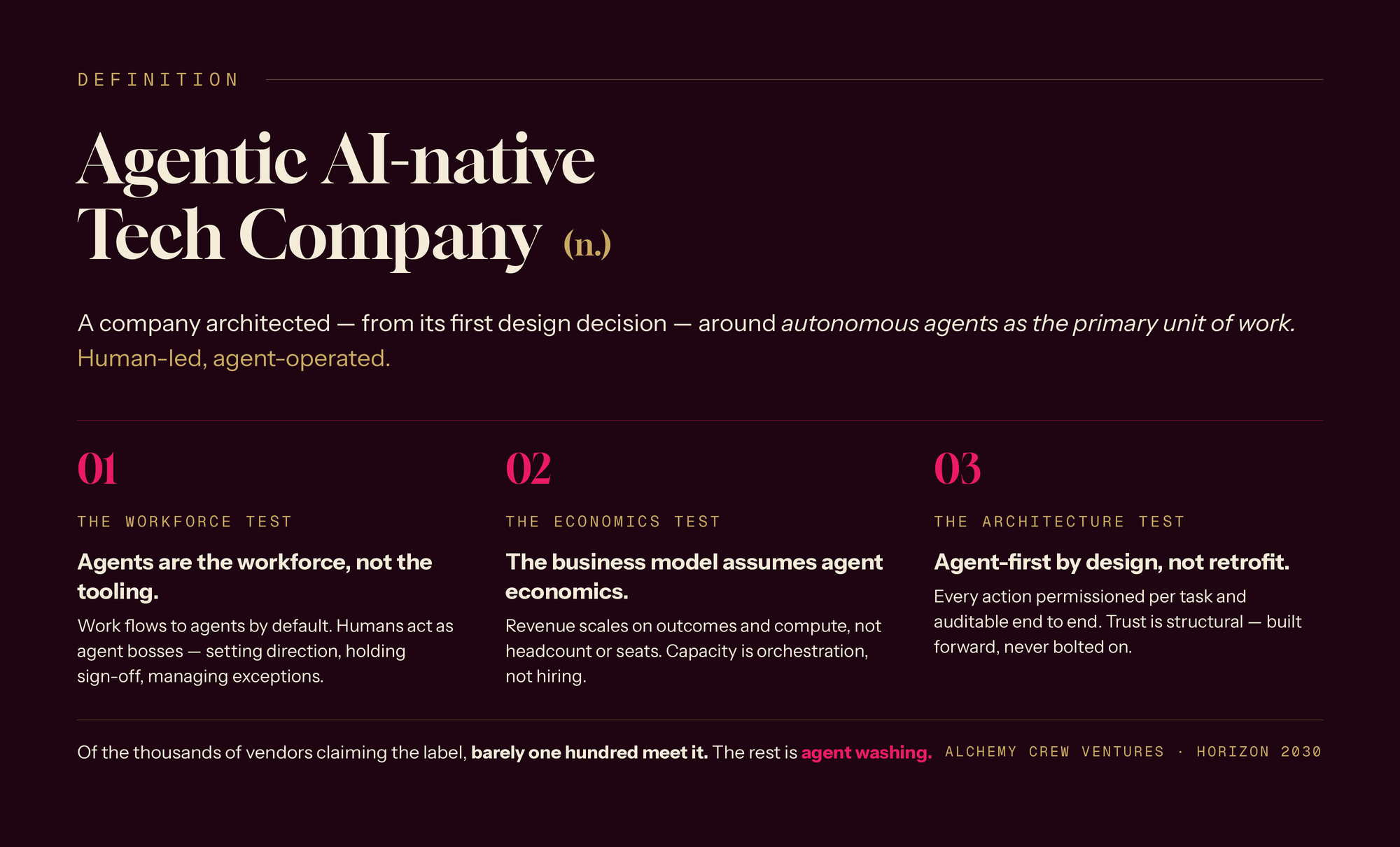

The agentic gold rush has a counterfeit problem. Thousands of vendors now claim the "agentic AI" label. Still, barely one hundred meet the definition. Gartner expects over 40% of agentic AI projects to be canceled by the end of 2027, not because agents don't work, but because organizations aren't structurally ready for them.

-

Readiness isn't a technology decision. It's an architecture decision. The Enterprise Intelligence Stack — human-led, agent-operated — sets the bar: agents as the primary unit of work, permissioned per task, and auditable end-to-end. Insurers that retrofit trust will lose to those who build it in.

-

The winning operating model won't hire more people; it will orchestrate digital labor. Allianz already runs seven agents for every human on its Nemo platform. The question for leaders isn't whether to deploy agents. It's whether your people are ready to become agent bosses.

Nine Months Ago, We Asked a Question. The Market Answered.

On 14 October 2025, fifty senior insurance leaders, investors, and innovators sat in a private room at Mandalay Bay and imagined an autonomous world. We asked what agentic AI in insurance would actually mean in practice: autonomous AI agents handling underwriting, claims, and other core insurer operations — and whether that would create efficiency or erode trust. We diagnosed why pilots fail — 95% of enterprise AI projects stalling, 73% of proofs-of-concept never reaching production, a $1.8 trillion protection gap widening while the industry experimented.

Nine months later, the diagnosis has been confirmed in the most public way possible. AI-focused ventures captured a record 95.2% of Q1 2026 InsurTech funding. Munich Re now sells parametric cover against AI failures. Zurich scaled Cytora's platform across five countries in ninety days. GEICO settled the first US regulatory case over an AI-driven cancellation process. Microsoft, AWS, OpenAI, and Anthropic committed $9 billion to embed engineers inside the Fortune 500, the venture-client model, industrialized. The autonomous world did not wait for 2030. It arrived early, unevenly, and without a manual.

And that unevenness is the story. Because underneath the deployment headlines sits a harder number, and it is the reason this article exists: by our current analysis, only around one in five insurers is structurally ready for agents. Not ready to pilot them — everyone can pilot. Ready to operate them: to permit them per task, audit them end to end, define human-agent roles, and hold a licensed human accountable at the moment of bind.

For C-suite insurance operators, reinsurers, brokers, investors, and AI-native scaleups trying to decide what scales, what governs, and what regulators will tolerate, this is a readiness problem before it is a technology story.

The ITC Vegas 2025 summit diagnosed why pilots fail. The question for 2026 is what the other four in five do next, and how an operating model such as the Enterprise Intelligence Stack closes the gap between experimentation and accountable deployment at scale.

What is the Readiness Problem?

The Readiness Problem is the widening gap between agentic AI adoption and operability: unlike traditional AI or task-specific AI tools, the issue is not using isolated capabilities but running full workflows reliably. Across the insurance industry, insurers are deploying agents faster than they are building the Frontier Operating Model — the data foundations, decision rights, and governance rails — required to run them accountably at scale, and to operate as a truly agentic frontier firm. Pilots don't scale; operating models do.

The Evidence: AI Adoption Is Sprinting. Readiness Is Walking.

Consider four signals from the past sixty days, each one a data point in the readiness ledger.

-

Agentic orchestration jumped from 5% to 25% of new insurer AI use cases in six months (Evident AI Index | Insurance, June 2026). A fivefold surge in adoption.

-

Yet only 8% of insurer AI use cases run end-to-end and demonstrably improve decision quality (Evident, June 2026, n=187). The other 92% remain assistive fragments: useful, unfinished, unaccountable.

-

Allianz's "Nemo" showed what disciplined autonomy looks like: seven agents prepare the work, one licensed human authorizes it. A 7:1 human-agent ratio with accountability by design, not by accident.

-

Liberty Mutual quotes now surface inside ChatGPT, with ACP rails from OpenAI and Stripe carrying checkout. Distribution has left the insurer's website and entered the agent economy, whether the rest of the operating model is ready or not.

Now set those signals against the macro forecast. McKinsey projects that agentic commerce and operations could generate $3–5 trillion in global revenue by 2030, and 81% of corporate leaders expect agents to be moderately or extensively integrated within 12 to 18 months.

Yet Gartner estimates over 40% of agentic AI projects will be canceled by the end of 2027 — victims of rising costs, unclear value, and inadequate risk controls. Of the thousands of vendors calling themselves agentic, analysts reckon barely a hundred meet the definition. The industry has a word for the rest: agent washing.

Both forecasts are right, and that is precisely the readiness problem. The trillions and the cancellations will happen to the same industry at the same time — sorted not by who adopted first, but by who built the operating model to hold what they adopted.

Adoption is a procurement decision. Readiness is an architecture decision. Confusing the two is how an insurer ends up with twenty-five pilots, zero production agents, and a board asking where the money went.

“Adoption is a procurement decision. Readiness is an architecture decision. Confusing the two is how you end up with twenty-five pilots and zero production agents.”

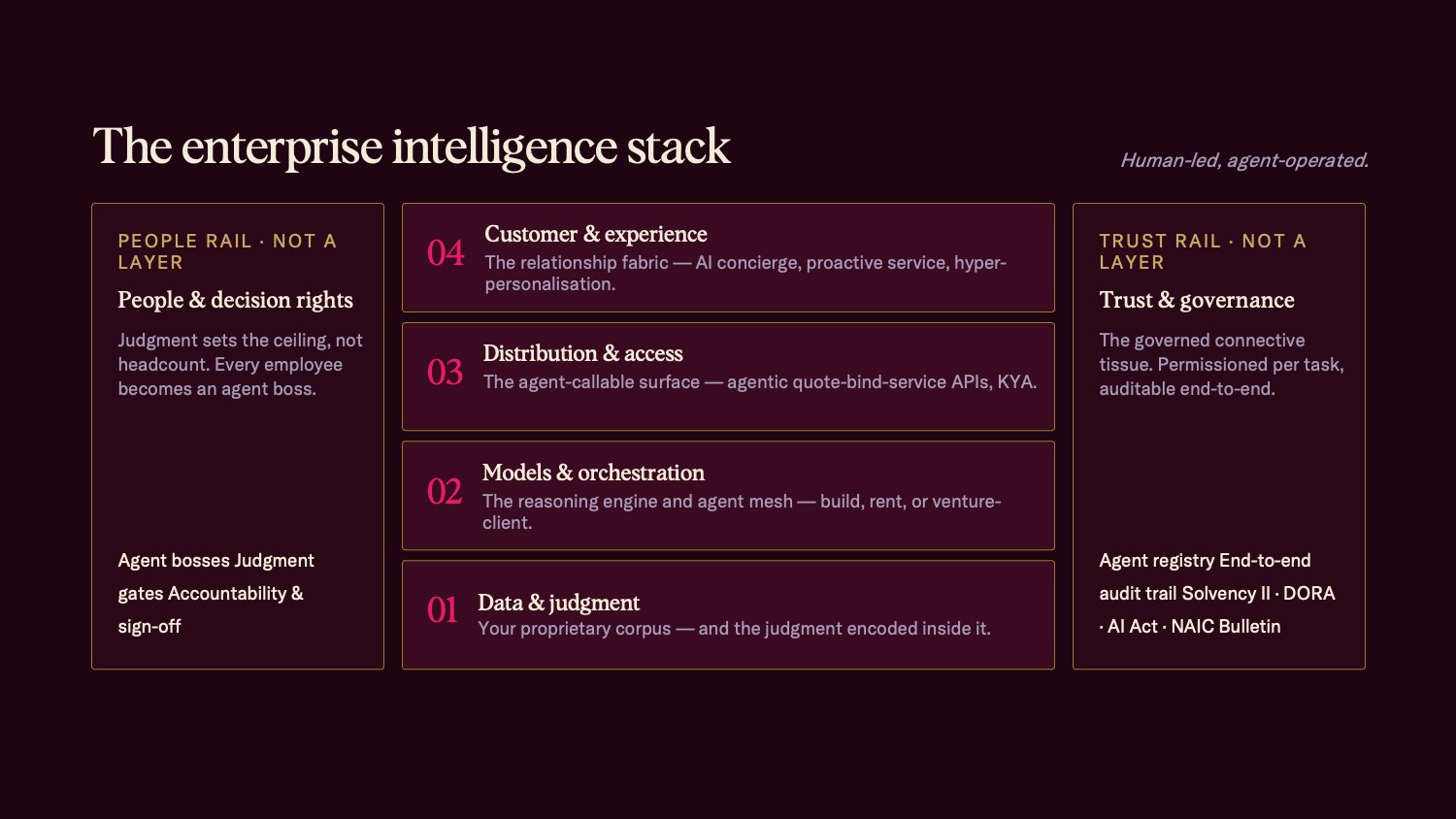

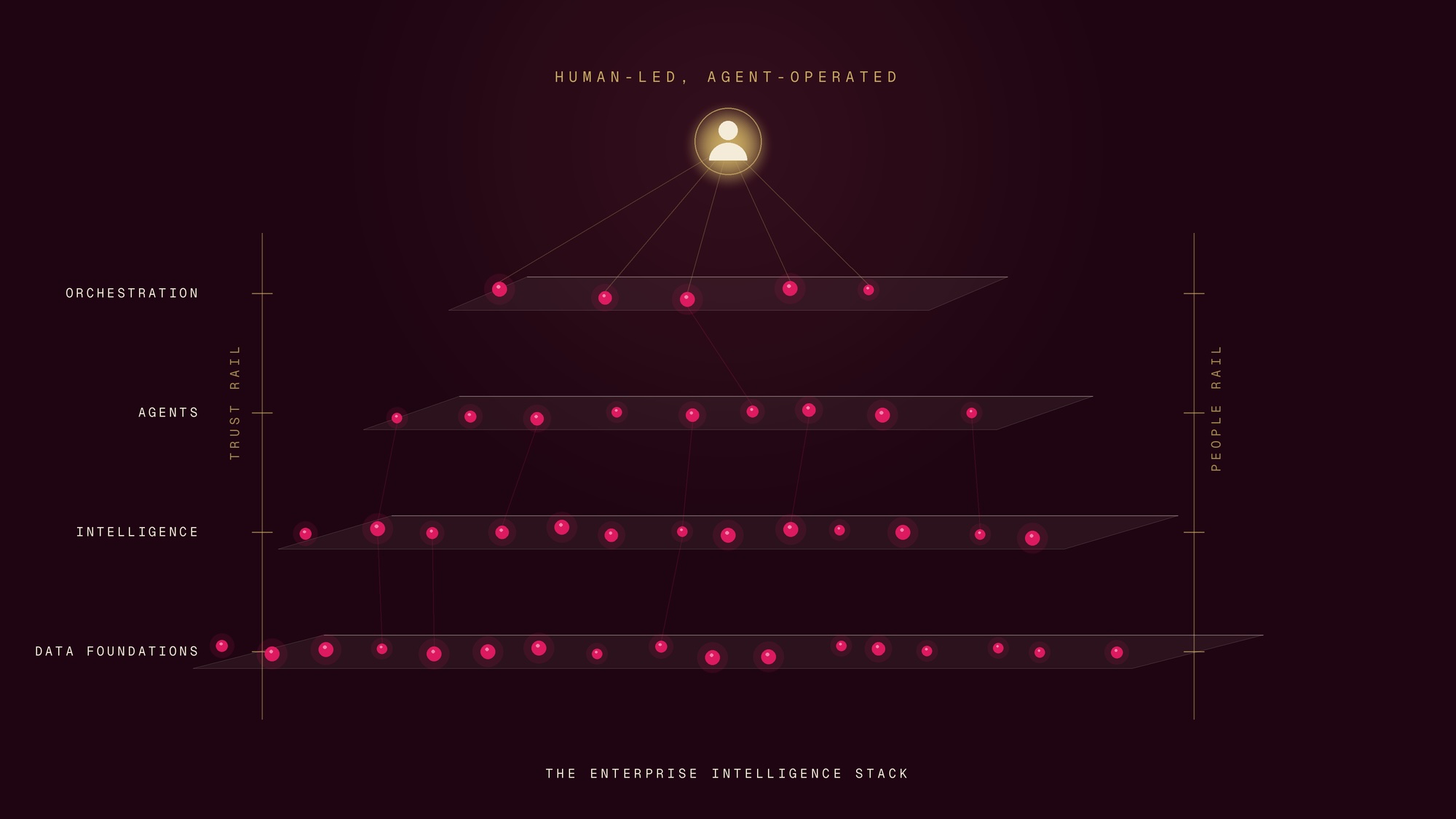

The Frontier Operating Model: Four Layers That Compound, Two Rails That Hold

Over the past nine months, working across our venture-client engagements and the signals we track weekly, we have been mapping what the structurally ready one-in-five actually have in common. The answer is not a technology choice. It is an architecture — what we call the Enterprise Intelligence Stack: human-led, agent-operated, built on four layers that compound value upward and two rails that hold the whole thing together. The most advanced frontier firms are the ones integrating AI into core business processes and business operations, not just pilots or standalone tools, behaving more like an AI-powered insurer than a traditional carrier experimenting at the edges.

The reframe that matters most: trust isn't a layer. People aren't a layer. They're the two rails every layer plugs into. The moment you treat governance as a checkbox stage or workforce change as a training module, the stack collapses. Treat them as rails — continuous, permissioned, accountable — and each layer caps the one above it: you cannot personalize what you cannot reach, reason over, or trust. And the path to that operating model typically moves through three phases of AI integration on the way to a Frontier Firm.

-

Layer 01 — Data & Judgment. Your proprietary corpus and the decisions encoded inside it. Not the data, the judgment within it: the knowledge graph, the judgment ledger, the feedback loops that turn thirty years of underwriting instinct into something an agent can learn from without leaking it to someone else's model. The question every board should ask: what sits on your intelligence-layer balance sheet, and whose model learns from it? For a carrier, this is the underwriting intelligence, loss, and pricing corpus. It is also where the industry's Data Trust Gap bites hardest: analysts still spend up to 75% of their capacity as data janitors, reconciling systems that were never designed to agree. Done well, real-time data supports more precise risk profiles and stronger risk assessment, and insurance agentic AI can improve underwriting accuracy by working across structured data and unstructured inputs, laying the foundation for Algorithmic Underwriting 2.0.

-

Layer 02 — Models & Orchestration. The reasoning engine and the agent mesh: sovereign and frontier models, tool connectors, evaluation and benchmarking, memory and context. The sourcing decision is made per task — build, rent, or venture-client — and it turns on one question: which decisions must never run on rented intelligence? Travelers answered by building TravelersLLM. Zurich answered by scaling Cytora. Neither answer is wrong; refusing to ask is. In practice, intelligent agents also support real-time portfolio monitoring for underwriters.

-

Layer 03 — Distribution & Access. The agent-callable surface: how you reach, and are reached by, the world's agents. Quote-bind-service APIs, agentic commerce, embedded cover at the point of need, discovery, and agent-readiness. Liberty Mutual's presence inside ChatGPT is the opening move of a much bigger game. The test: can an outside agent discover you, quote you, and transact — safely? Insurers who cannot answer will become invisible to the algorithmic delegates increasingly making buying decisions — a protection gap of a new kind, created not by unaffordability but by undiscoverability.

-

Layer 04 — Customer & Experience. The edge: AI concierges, proactive service, in-life ecosystem services, hyper-personalization, human-agent support. This is where infrastructure becomes the human prize, and where the most generous question in insurance finally becomes economical: who can you now afford to serve that you couldn't yesterday? The layers below decide the answer. That is what compounding means.

-

The People Rail — People & Decision Rights. Judgment sets the ceiling, not headcount. Every employee becomes an agent boss: setting direction, holding sign-off, managing exceptions, escalating edge cases. Allianz's 7:1 Nemo ratio is this rail made visible, underwriters and adjusters as agent bosses, with delegated authority defined at the moment of bind. The rail also carries the cultural work: dismantling the fear of obsolescence, rewarding people for orchestrating digital labor well, and paying down the verification tax, or the hours humans burn double-checking AI output they haven't yet earned reasons to trust.

-

The Trust Rail — Trust & Governance. The governed connective tissue: permissioned per task, auditable end to end. Agent registries and guardrails, data contracts and lineage, risk sensing, regulatory overlay, ethics and human oversight. In a highly regulated industry, effective implementation also requires regulatory compliance, clear governance frameworks, and robust data governance. For insurers, the overlay is concrete — Solvency II, DORA, EIOPA's consultation cadence, the EU AI Act's deferred-but-inevitable high-risk regime — and the operating principle is simple: a human authorizes at bind. The GEICO settlement showed what happens when this rail is missing. Aviva's £233 million in AI-abused fraud showed the rail must face outward too.

The Messy Middle Is Where the Other Four in Five Live

Between today's pilot estate and the human-led, agent-operated firm sits what we have been calling the messy middle: enterprise debt, undocumented workarounds, tacit knowledge locked in the heads of a retiring workforce, and legacy systems that answer an executive's Tuesday-morning question three days late with data that expired on Monday. This is not a detour on the way to readiness. It is the work itself.

The ready one-in-five did not skip the messy middle; they industrialized their way through it. They captured tacit judgment into the foundation before the people holding it retired. They set autonomy states deliberately — human-led, human-agent, agent-run — per workflow, with 2028 targets scored quarterly rather than aspirations announced annually. They ran venture-client pilots that graduated on evidence: cycle time, leakage, loss ratio, and decision quality. In underwriting, platform adoption has produced measurable improvements, including 3–5 percentage-point loss ratio improvements and lower operational costs. That is the real shift: moving from pilot projects to workflows tied to measurable gains, where AI is transforming insurance underwriting and embedded agentic AI can improve underwriting profit by $40 million annually, reduce administrative costs, and accelerate turnaround times. And they accepted the uncomfortable sequencing truth the stack imposes: the least glamorous layer, data and judgment, caps everything above it. There is no shortcut to the edge.

Announcing the 2026 Summit — Horizon 2030: The Readiness Problem

This is the conversation we are convening on the kickoff day of ITC Vegas 2026, in the same format that made the 2025 summit work: roughly fifty senior leaders — CVCs and venture investors, insurers and reinsurers, brokers, AI-native scaleups — in a private room at Mandalay Bay, under Chatham House rules, with live polling keeping everyone honest.

Horizon 2030: The Readiness Problem is the successor session to AI Horizons 2030: Provocations and Possibilities. Where 2025 diagnosed why pilots fail, 2026 addresses the operating-model decision that follows. The afternoon runs three lenses in sequence — the investor lens, the insurer lens, the tech lens — mirroring the three perspectives that shaped the original summit, then closes with a structured roundtable workshop discussion where the room does what this industry does best when the doors are shut: learns from itself. I will open with the readiness gap and close with the verdict the room has argued its way to.

Anchoring the session are the preliminary findings from our Alchemy Crew Frontier Insurer Index — our readiness benchmark for the agentic era, in development with Bayes Business School for release in 2027. The Index measures what this article has argued: architecture, human-agent ratio, decision quality, distribution sovereignty, governance spine, capital posture, and connects to a broader view of scaling with technologies across insurance and adjacent industries.

The one-in-five headline will be restated to the Index's fielded number ahead of the event; the framing is deliberately robust to that restatement. Whichever way the decimal falls, the strategic question stands: what do the other four do?

Attendance is invitation-only and curated, as it was in 2025. If you lead an insurer, invest in the category, or build the technology this article describes — and you want to be in the room where the readiness conversation gets specific, and to compare notes with insights from the Global Insurtech Summit on the industry’s digital future: request an invitation. The provocations of 2025 became the operating agenda of 2026. The 2026 room writes the agenda for 2027.

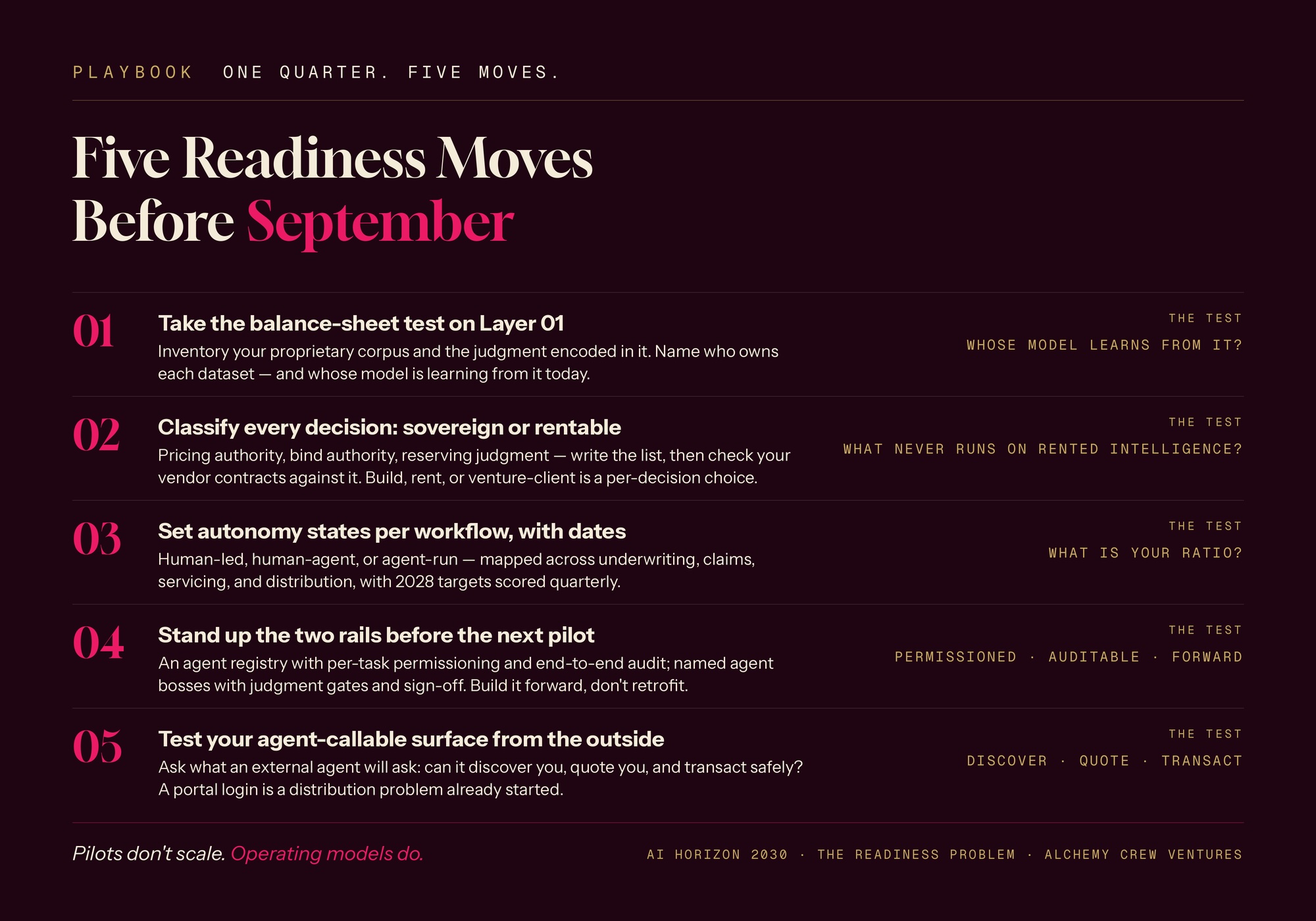

Five Readiness Moves Before September

You do not need the summit to start. Five moves, one quarter:

-

Take the balance-sheet test on Layer 01. Inventory your proprietary corpus and the judgment encoded in it. Name what sits on your intelligence-layer balance sheet, who owns each dataset, and whose model is learning from it today. If the answer to the last question includes vendors, you have found your first governance gap.

-

Classify every decision as sovereign or rentable. Which decisions must never run on rented intelligence — pricing authority, bind authority, reserving judgment? Write the list, then check your current vendor contracts against it. Build, rent, or venture-client is a per-decision choice, not an enterprise religion.

-

Set your autonomy states per workflow, with dates. Human-led, human-agent, or agent-run — mapped across underwriting, claims, servicing, and distribution, with explicit 2028 targets and quarterly scoring. Allianz's 7:1 is a benchmark, not a rule; having no ratio at all is the failure mode, and implementing agentic AI can cut quote preparation from hours to minutes while lifting underwriting quote capacity by 40%.

-

Stand up the two rails before the next pilot. An agent registry with per-task permissioning and an end-to-end audit trail on the trust side; named agent bosses with judgment gates and sign-off authority on the people side. These intelligent systems can automate high-volume claims processing and data extraction, and AI systems can take over routine tasks such as data entry and document verification with less manual intervention. With governance and human review checkpoints in place, they can handle double the claims volume without extra staff, while human judgment stays with the people who approve outcomes and humans focus on exceptions.

-

Test your agent-callable surface from the outside. Ask the question an external agent will ask: can it discover you, quote you, and transact safely? If Liberty Mutual's quotes reach customers inside ChatGPT and yours require a portal login, your distribution problem has already started.

The Stakes, One Year On

Last November, I wrote that 2030 AI horizons aren't fixed; they're co-creatable, and that the industry's mood had matured into urgency plus agency. The past nine months added the third ingredient: architecture.

The gap between the one in five and everyone else is not a gap in ambition, budget, or awareness. It is a gap in the operating model. Insurers that embed artificial intelligence into their operations create real value, including 10–15% increases in new-business premiums. When done well, AI transformation also supports 3–5 percentage-point improvements in loss ratio. It compounds quarterly in expense ratios, in talent, in regulatory readiness, in who the world's agents can even find, especially for carriers building a digital workforce of humans and AI together.

The insurers who spend the next twelve months building layers and rails will spend 2028 answering the generous question: who can we now afford to serve? The insurers who spend it piloting will spend 2028 explaining variance.

Pilots don't scale. Operating models do. See you in Vegas.

Horizon 2030: The Readiness Problem — invitation-only executive summit, kickoff day of ITC Vegas 2026, Mandalay Bay, Las Vegas. Request an invitation: [email protected]. Sponsorship inquiries welcome.

FAQ: The Readiness Problem

What is the Enterprise Intelligence Stack?

A human-led, agent-operated architecture of four compounding layers — Data & Judgment, Models & Orchestration, Distribution & Access, Customer & Experience — anchored by two horizontal rails: People & Decision Rights and Trust & Governance. Each layer is capped by the one beneath it; the rails run continuously through all four, supporting more complex decision-making than task-specific systems and distinguishing this stack from generative AI used on its own.

Why aren't trust and people layers?

Because layers are stages you complete, rails are surfaces you are accountable to continuously. Every autonomous action must be permissioned per task and auditable end to end (trust rail), and a human must hold sign-off authority, however much is agent-executed, with Human Review acting as the control point that validates AI-led decision-making before finalization in governed workflows (people rail). A human authorizes at bind.

What does 'structurally ready for agents' mean?

An insurer that can operate agents, not just pilot them: a governed data-and-judgment foundation, deliberate sovereign-versus-rented model choices, an agent-callable distribution surface, defined autonomy states per workflow, named agent bosses with judgment gates, per-task permissioning with end-to-end audit, the ability to connect fragmented systems and turn submissions into structured data for accurate risk assessment, and readiness that means adopting ai beyond pilots and embedding it into core business processes. Current analysis suggests roughly one in five insurers meets that bar, even as the broader digital transformation of insurance accelerates around them.

What is an agent boss?

The elevated role every employee assumes in a Frontier Firm: setting direction for a portfolio of AI agents, holding accountability and sign-off, managing exceptions and escalations. Judgment sets the ceiling, not headcount — Allianz's Nemo runs seven agents to one licensed human authorizer.

Is agentic adoption actually accelerating in insurance?

Yes — agentic orchestration grew from 5% to 25% of new insurer AI use cases in six months (Evident AI Index | Insurance, June 2026). But only 8% of insurer AI use cases run end-to-end and improve decision quality (n=187). The adoption curve is steep; the readiness curve is flat. That divergence is the Readiness Problem. In many organizations, the gap appears when AI remains in pilots rather than being built into core workflows. What counts now is measured digital transformation: where teams once focused on cloud migration, they now focus on how work is supported by multiple AI agents. Increasingly, that includes generative AI agents as part of scaled deployment rather than experimentation.

What is the Frontier Insurer Index?

Alchemy Crew's readiness benchmark for the agentic era, in development with Bayes Business School for release in 2027. It scores insurers across architecture, human-agent ratio, decision quality, distribution sovereignty, governance spine, and capital posture and anchors the Horizon 2030 summit's headline findings.

What is Horizon 2030: The Readiness Problem?

An invitation-only executive summit on the kickoff day of ITC Vegas 2026 at Mandalay Bay — the successor to AI Horizons 2030 (October 2025). Around fifty senior leaders, three panels (investor, insurer, tech lenses), live polling, and a structured roundtable, under Chatham House rules, followed by a published synthesis article.

Won't most agentic projects fail anyway?

Many will: Gartner projects over 40% of agentic AI projects will be canceled by the end of 2027, and agent washing is rife — of thousands of self-described agentic vendors, barely a hundred meet the definition. That is an argument for readiness, not against agents: the cancellations will concentrate among firms that adopted without an operating model, treating AI tools or intelligent assistants as isolated experiments instead of a governed digital leadership response, as explored in why your AI strategy is failing and your startup is stalling, which is where firms move from isolated adoption to true digital transformation and get real value.

Sources and Signals

This article draws on the Alchemy Crew Content Signal Hub (234 signals, May–July 2026), the Evident AI Index | Insurance (June 2026), Gallagher Re Global InsurTech Reports (FY2025–Q1 2026), Gartner and McKinsey agentic-AI analyses, MIT NANDA, the Enterprise Intelligence Stack research programme (Alchemy Crew Ventures, 2026), and primary announcements from Allianz, Liberty Mutual, Munich Re, Zurich, Travelers, Aviva, and GEICO regulatory filings. The Frontier Insurer Index is developed with Bayes Business School for release in 2027.

Editor in Chief

Rebuilding Risk Resilience