CUO White Paper: Risk Futures Begin with the Data Underwriters Don't Have

May 15, 2026

Written by Sabine VanderLinden

What this white paper commissioned by Anthony Peake from Intelligent AI reveals about the £368B Protection Gap — and the Frontier Operating Model that closes it.

|

Key Takeaways

|

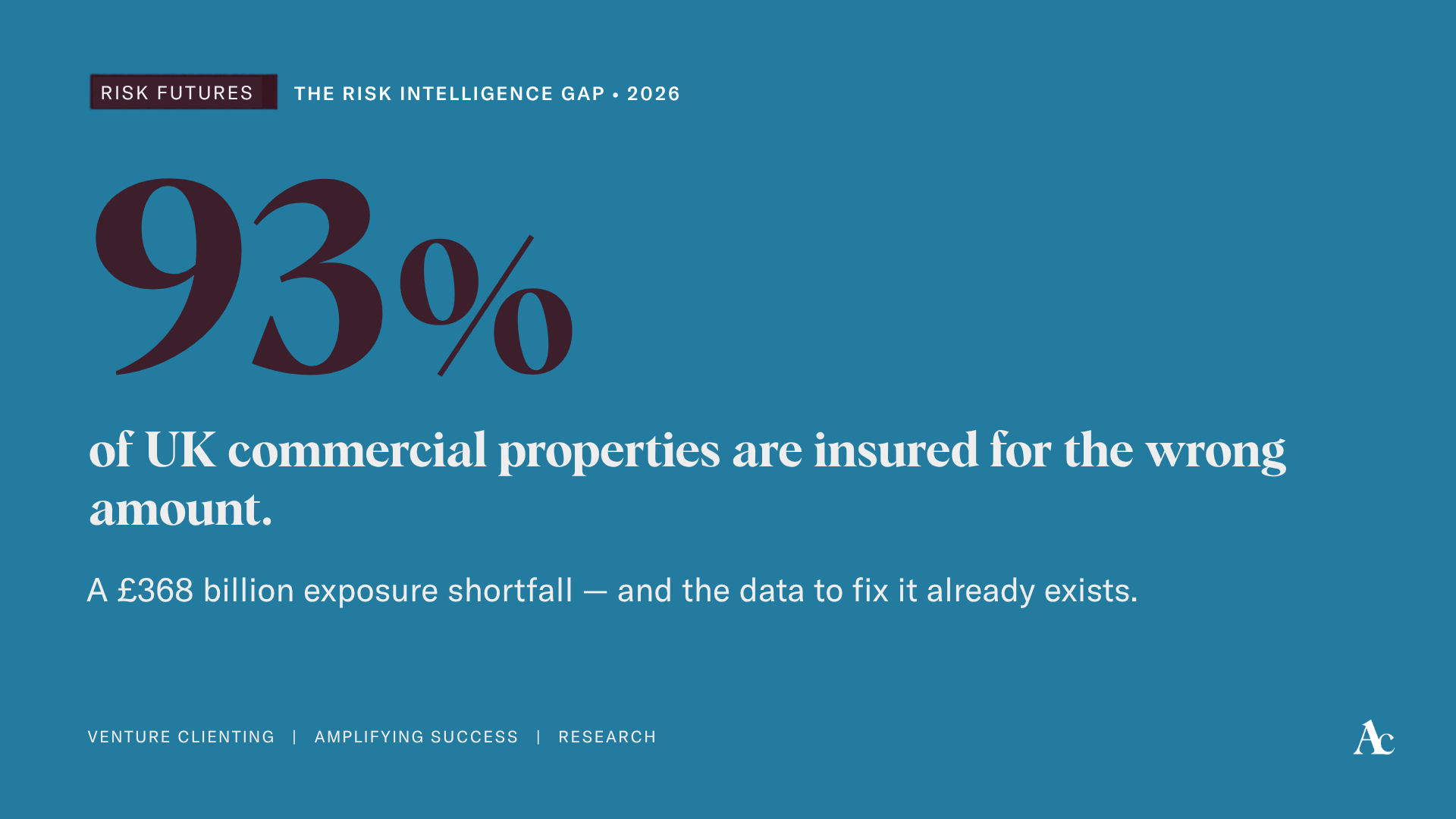

Ninety-three percent. That is the proportion of UK commercial properties insured for the wrong amount. Across the Atlantic, 90% of US commercial buildings have inadequate coverage. The underwriters, the people whose decisions the entire system rests on, rate their access to risk intelligence at 3 to 5 out of ten at the moment of bind. This is the front line of Risk Futures, and it is fragile.

In 2024, global insured catastrophe losses reached $145 billion. The US Property and Casualty industry posted consecutive net underwriting losses exceeding $20 billion in both 2022 and 2023. The industry has poured billions into AI pricing engines and catastrophe models. What fuel feeds those engines? Stale. Unverified. Often wrong. Better engines running on worse fuel — that is the Risk Futures paradox sitting at the center of every commercial property book today.

I have spent three months (Jan–March 2026) co-authoring a new research paper with Anthony Peake, CEO of Intelligent AI, The Risk Intelligence Gap: How Exposure Data Deficiency is Reshaping Property Underwriting. The paper draws on more than 30 insurers’ annual reports, 20 executive interviews, and multiple streams of secondary research. The findings are not subtle. They are structural.

What is the Risk Intelligence Gap?

The Risk Intelligence Gap is the structural distance between the data the property insurance ecosystem already holds and the verified, structured, decision-grade intelligence underwriters can use at the point of bind. It is not a data shortage — it is an architecture problem, an integration problem, and fundamentally a trust problem.

Closing it is the foundation of any credible Risk Futures strategy.

The Architecture Problem Behind The Protection Gap

We tend to talk about The Protection Gap as a coverage problem. It is not. It is a data problem wearing a coverage costume.

In the UK alone, 70% of commercial property is materially underinsured, a cumulative exposure shortfall of more than £368 billion. In the United States, 90% of commercial buildings carry inadequate coverage, and after the January 2025 Los Angeles wildfires destroyed 17,000 structures, many of those policies were based on outdated baselines. Construction, plant, and labor costs rose by roughly 20% last year. Most portfolios were adjusted by one to three.

Why? Because the data exists, but it does not flow. Less than 50% of properties in a typical insurer’s portfolio carry a usable address. Risk engineers visit 3% to 5% of sites, 20% in the most technically rigorous carriers. The COPE model — Construction, Occupancy, Protection, Environment — calls for around one hundred data points per building. In practice, underwriters work from a fraction.

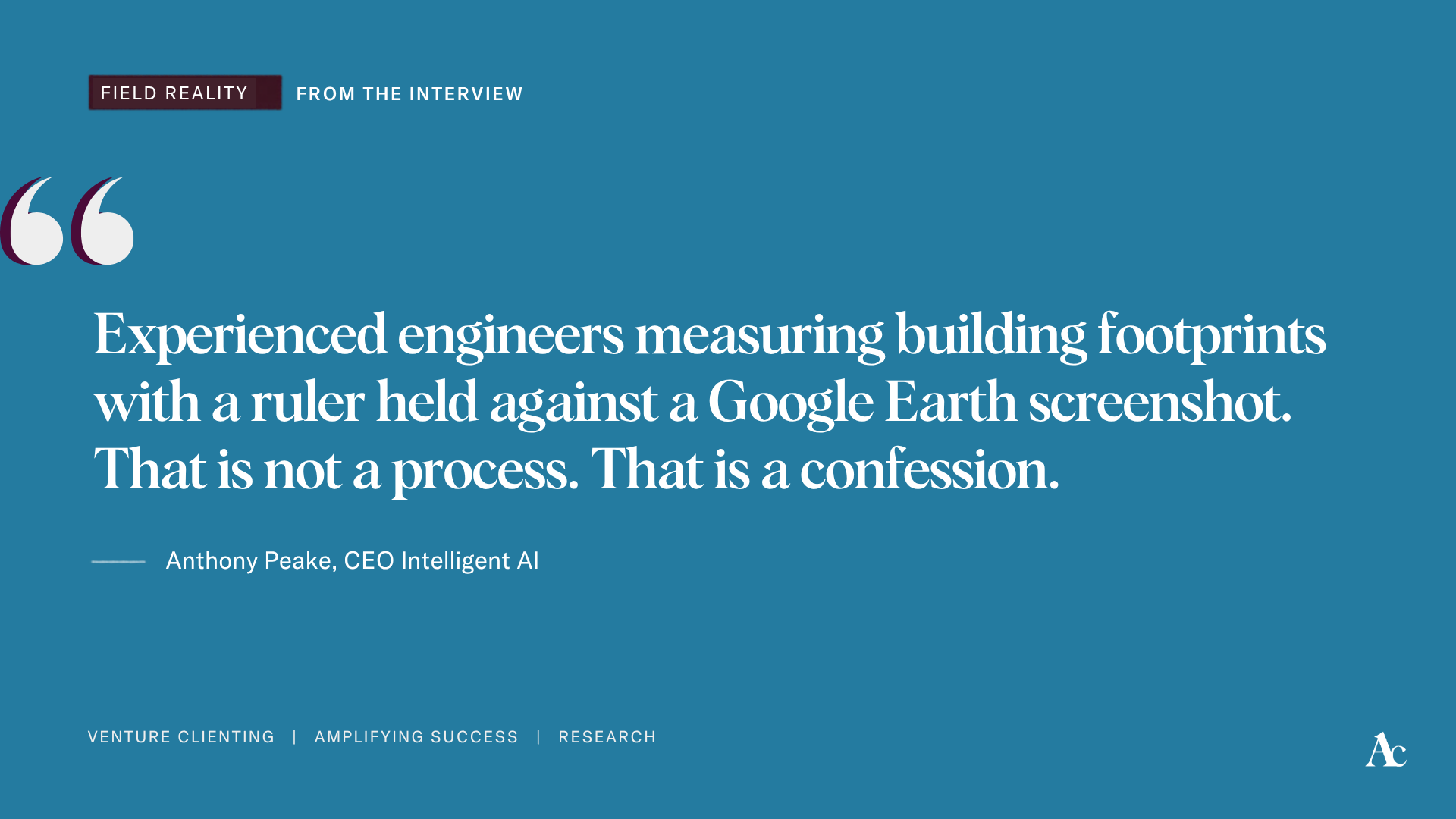

I watched Anthony describe what this looks like in the field: experienced engineers measuring building footprints with a ruler held against a Google Earth screenshot. That is not a process. That is a confession.

He shared one US case in which a portfolio site, insured for $85 million as a “well-managed, fully sprinklered storage facility,” turned out to be a 14,000-square-meter chicken rendering plant — 52% sprinklered, with four prior flood incidents and over $10 million in pollution fines. The actual loss exposure: $250 million. The carrier was making billion-dollar decisions on thousand-dollar data. That is where Risk Futures meets reality.

The Hidden Data Tax That Breaks the Frontier Operating Model

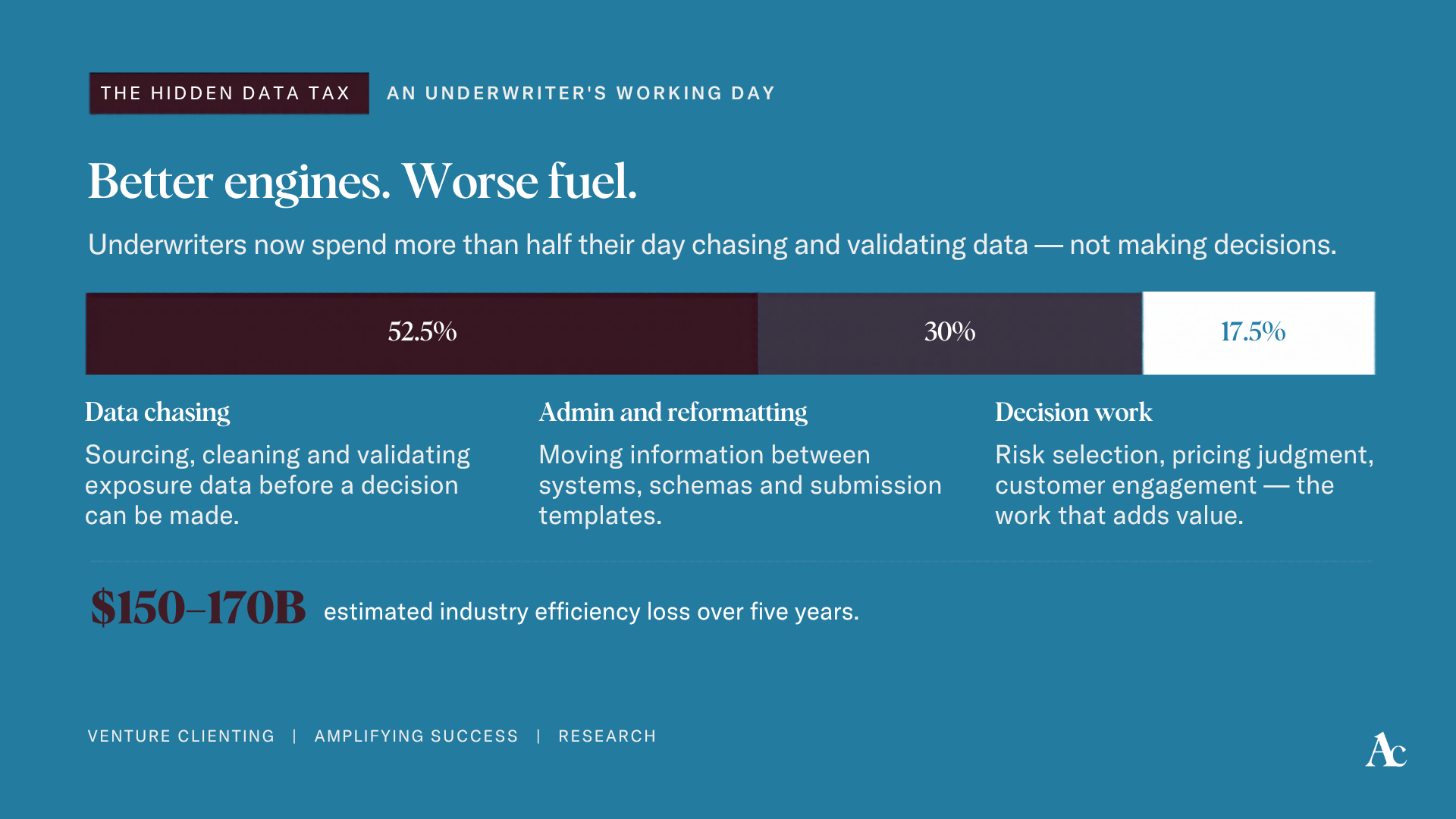

Underwriters now spend 50% to 55% of their working day chasing, validating, and reformatting data — not making decisions. Across the industry, that is an estimated $150–$170 billion in efficiency loss over five years. This is the hidden data tax, and it is the single largest blocker to a credible Frontier Operating Model in commercial property insurance.

A Frontier Operating Model is one in which every human is an agent manager, every workflow is augmented by verified intelligence, and every decision is made at machine speed, with human judgment on top. It is the operating layer that enables a carrier to write three times the volume with the same headcount, with sharper risk selection, and a defensible audit trail. It does not work on broken inputs. It cannot.

Anthony shared a case that makes this concrete. One insurer needed 10,000 site surveys a year. Maximum capacity, even with everyone healthy and on the job, was 5,000. Working with Intelligent AI, they triaged 7,000 of those digitally, freeing risk engineers to do 3,000 high-value visits with twice as much time per client. Same team. Twice the work. Better risk selection. More capacity for growth. This is what digital labor looks like when it is engineered into the workflow rather than bolted onto it.

80% of what humans do in property underwriting today is administrative work. Less than 20% adds value to the customer or the business. Halve the admin, and you double the value. That is not optimization. That is structural workforce transformation.

The Intelligence Layer: From Asserted Data to Verified Intelligence

The fix is not a better model. It is a better fuel system.

What Anthony and his team have built — and what the paper documents — is the missing Insurance Intelligence Layer for commercial property: a verified, API-first data foundation covering more than one hundred structured data points per building, sourced from satellite imagery, tax records, GIS polygons, IoT sensors, and historical claims, with three independent sources behind every data point and an algorithmic confidence score attached to each.

That last detail matters. Underwriters told us, repeatedly, that they will not act on data they cannot explain. So the Intelligence Layer cannot pretend to be perfect. It has to be honest. This attribute is 98.2% accurate. This one is 72%. Here are the sources. Here are the dates. Here is the work in progress. That is what builds trust. Not the assertion. The audit trail.

The shift the paper describes is from asserted data to verified intelligence, from periodic snapshots to continuous monitoring, from reactive data chasing to decision-grade insight at the point of bind. Discoverable. Quotable. Bindable. Three properties every Chief Underwriting Officer needs from their data foundation, and three properties most CUOs cannot honestly claim today. The Risk Futures discipline starts here, or it does not start at all.

Better Engines, or Better Fuel?

This is the contrast every board is now wrestling with. Carriers have spent a decade investing in better engines: pricing, cat modeling, portfolio optimization, and generative AI for submission triage. The underlying assumption was that better algorithms would compensate for input noise. They have not. They cannot.

The Lloyd’s portfolio Anthony recently re-priced makes the point. 355 commercial properties, insured for £5 billion, should have been insured for £6.17 billion. The carrier was collecting £7.5 million in premiums against an actual exposure of £10 million. Not a fringe portfolio. A fairly clean one. Multiply that across the 355,000-property portfolios that mid-sized commercial carriers run, and the gap is not a rounding error. It is the difference between underwriting profit and consecutive years of red ink.

What separates a Risk Futures-led carrier from a slow adopter is no longer algorithmic sophistication. It is the quality of the fuel.

The CUO Playbook: Five Moves for the Next 90 Days

If you are a Chief Underwriting Officer reading this on a Monday morning, the white paper sets out the full implementation roadmap. Here is the compressed version — your Risk Futures playbook for the next quarter.

- Audit your address quality. Run a sample of one thousand in-force commercial policies and measure how many resolve to a verified, geocoded address. If it is below 70%, every downstream data exercise is compromised.

- Re-price one underperforming portfolio against a verified COPE baseline. Do not run it across the book — pick the weakest. The premium uplift and the risk re-selection signal will tell you the size of your gap in two weeks.

- Replace at least one annual physical survey cycle with a digital triage layer. Free your risk engineers to spend twice as long with the clients who genuinely need them.

- Demand confidence scores on every third-party data feed. Refuse to act on a data point without a source, a date, and an algorithmic confidence rating. Make it a procurement standard.

- Treat the Intelligence Layer as infrastructure, not a vendor decision. It sits beneath your pricing engine, cat model, submission system, and claims platform. If it is not API-first and shareable across that stack, it is not infrastructure.

What Happens If You Wait

The next extreme weather season will not wait for your data. The Financial Conduct Authority’s Consumer Duty Act has already triggered a 400% increase in complaints against carriers that hide behind averaging clauses. Guidewire — the platform behind 540 of the largest insurers globally — has just integrated Intelligent AI’s Risk API into its ecosystem. The Frontier Insurer is no longer a future construct. It is being built right now by the carriers who decided that the data foundation matters more than the next pricing model.

Risk Futures is no longer optional. The question is not whether the Risk Intelligence Gap closes — it is closing. The question is who closes it on their own terms, and who closes it after a $250-million surprise on a portfolio they thought they understood.

Make sure to download The Risk Intelligence Gap Report.

The Risk Intelligence Gap: How Exposure Data Deficiency is Reshaping Property Underwriting is now available. Forty pages. Twenty executive interviews. The full evidence base, the cross-Atlantic comparison, and the implementation roadmap that turns Risk Futures from a slogan into a quarter-by-quarter discipline.

If your portfolio is built on data that would not pass a first-year audit, this paper is for you.

Frequently Asked Questions

What is the Risk Intelligence Gap in property underwriting?

The Risk Intelligence Gap is the structural distance between the data the property insurance ecosystem already holds and the verified, structured intelligence underwriters can use at the point of bind. It is an architecture and trust problem, not a data shortage, and closing it is the foundation of any credible Risk Futures strategy.

How under-insured are UK and US commercial properties?

Roughly 93% of UK commercial properties are insured for the wrong amount, with 70% materially under-insured and a cumulative exposure shortfall of more than £368 billion. In the United States, around 90% of commercial buildings carry inadequate cover. Globally, an estimated 80% of properties are under-insured by at least 50%.

What is the COPE model in property underwriting?

COPE stands for Construction, Occupancy, Protection, and Environment. It is the canonical schema for assessing commercial property risk — wall, roof, and frame materials, building use, sprinklers and alarms, and natural-catastrophe exposure. Each insurer needs roughly 100 COPE data points per building to underwrite with confidence. Most carriers work from a fraction.

What is an Insurance Intelligence Layer?

An Insurance Intelligence Layer is a verified, API-first data foundation that delivers structured, source-attributed risk data into underwriting, claims, and pricing systems at the point of decision. Each data point carries three independent sources, a date, and an algorithmic confidence score. It converts asserted data into decision-grade Digital Risk Intelligence — and it is the precondition for a credible Frontier Operating Model.

What can a Chief Underwriting Officer do in the next ninety days to close the Risk Intelligence Gap?

Audit address quality across a thousand in-force policies, reprice one underperforming portfolio against a verified COPE baseline, replace one annual physical survey cycle with digital triage, demand confidence scores for every third-party data feed, and treat the Intelligence Layer as infrastructure rather than a vendor decision.

Why does the Risk Intelligence Gap matter for a Frontier Operating Model?

A Frontier Operating Model requires every human to operate as an agent manager, supervising AI-augmented workflows at machine speed with human judgment on top. That model cannot run on stale, unverified data. The Risk Intelligence Gap is the single largest structural blocker to building a Frontier Insurer in commercial property — close it, and the rest of the operating model becomes engineering. Leave it open, and every downstream AI investment compounds the noise instead of the signal.

Listen to the Interview with Anthony Peake

The Risk Intelligence Gap: How Exposure Data Deficiency Is Reshaping Property Underwriting

In this episode of the Scouting for Growth podcast, Anthony Peake, CEO of Intelligent AI, and I discuss the “Risk Intelligence Gap” reshaping the property insurance landscape. We are both dissecting the recent white paper Anthony commissioned during Q1 2026.

Editor in Chief

Rebuilding Risk Resilience